Meta Bets the Farm, Apple Milks the Cows

It was a tale of two quarterly reports. While both Meta and Apple posted incredible numbers, Wall Street had a very different reaction to each. Meta shares surged after their earnings numbers came in, while Apple has fluctuated between being up and down ever-so-slightly. And the reasons would seem to be related.

Meta, perhaps more so than any other company in the Big Tech cohort gets hit constantly by Wall Street depending on the details in these reports. That's in no small part because Mark Zuckerberg has proven himself to be super aggressive when it comes to new initiatives. As a founder with total control of his company, he can afford to do this, quite literally, but that doesn't mean Wall Street is going to like it. In fact, they often hate it. And they're often not wrong.

The Reality Labs division is a good example of this. Over the past many years, Zuck has burned tens of billions of dollars with little to show for it. Sure, there are the Ray-Ban Meta smart glasses, but the company could have undoubtedly made those at a fraction of the spend. Most of the money, of course, was spent on the Metaverse. That is, trying to make VR happen for about the tenth time in the past few decades. Once again, it hasn't worked – even with Apple entering the space to "validate" Meta's spend, not to mention name change.

Part of the reason why investors were pleased with Meta this week is undoubtedly because the company has finally acknowledged the reality of Reality Labs. They've started cutting jobs to literally cut their losses, and Zuck is now saying this year will be the peak of that division's burn as they unwind from VR to focus on future smart glasses and mobile and yes, AI.

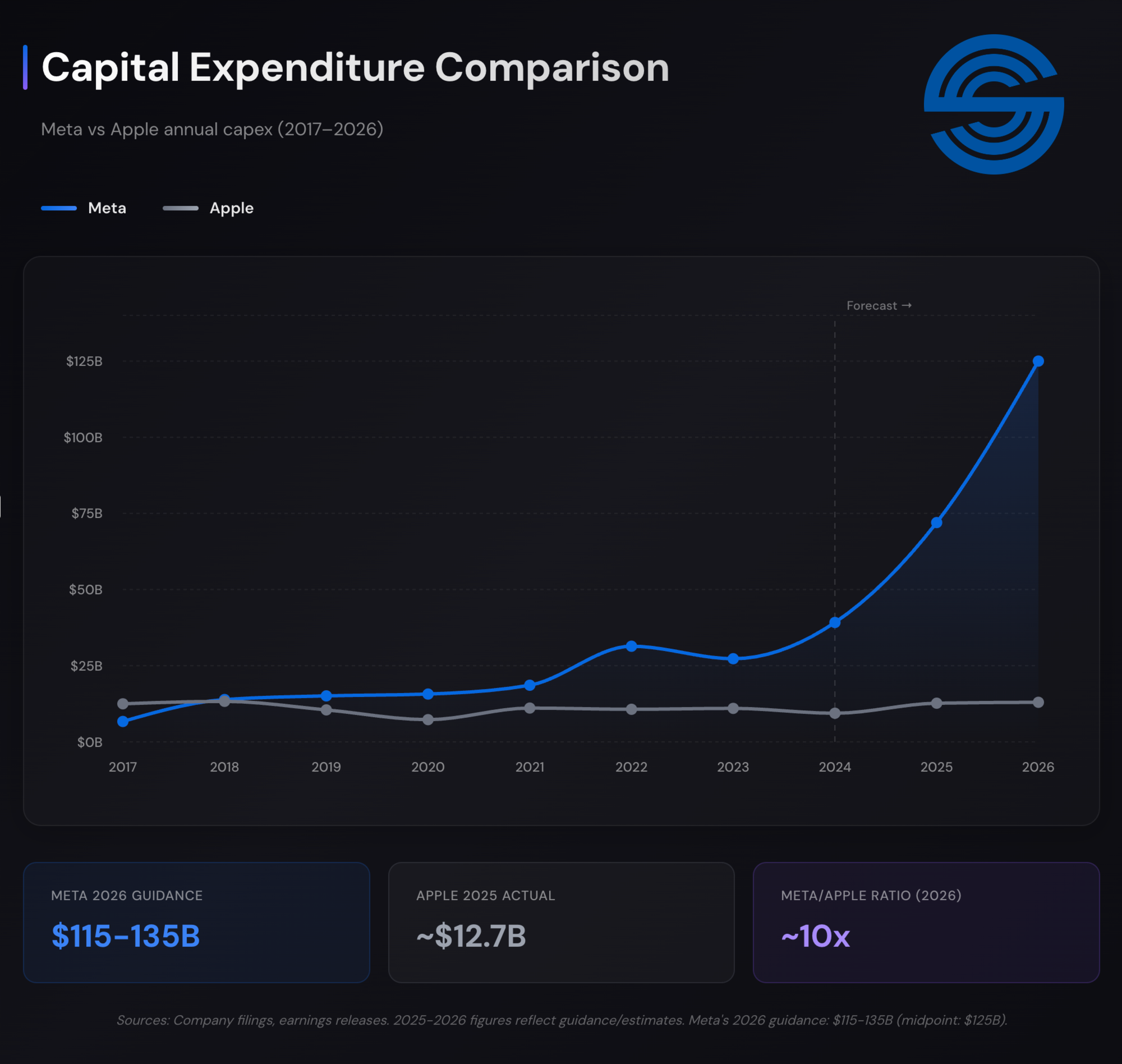

Speaking of, beyond the Reality Labs spend, what Wall Street has hated about Meta from a stock perspective in recent quarters was the massive ramp in CapEx. Obviously, the combination of the two was too much for investors' taste. Not helping matters was the fact that Meta clearly made some big mistakes with their initial foray into AI and had to reset the entire effort – for the low, low cost of tens of billions of dollars.

Anyway, with these reboots/restructures now seemingly in the rearview, Meta may be getting a new lease on life from a Wall Street perspective. The most incredible thing about this quarter wasn't Meta's impressive earnings, it was how after they disclosed an even larger ramp in CapEx spend – truly incredible given that they're up near the top versus their peers and yet they don't have actual third-party cloud businesses to maintain – investors not only didn't throw up all over it, they ate it up!

Again, part of it is the newfound belief that Zuck will ultimately do the "right thing" if his spend isn't working. And part of it is the fact that the underlying ads business continues to be able to more than cover such costs. And it's the belief that AI actually does seem to help that core business. But still, you probably don't need to spend quite so much money relative to your peer group to get those results. Zuck, as he's made abundantly clear, is going all-in on AI not just to serve better ads, but to serve up the future to the world.

As relayed by Ben Thompson from his write-up on Meta's earnings, this was the most interesting answer Zuck gave during the call with investors:

I think the question was around how important is it for us to have a general model. The way that I think about Meta is we’re a deep technology company. Some people think about us as we build these apps and experiences, but the thing that allows us to build all these things is that we build and control the underlying technology that allows us to integrate and design the experiences that we want and not just be constrained to what others in the ecosystem are building or allow us to build.

So I think that this is a really fundamental thing where my guess is that frontier AI for many reasons, some competitive, some safety oriented, are not going to always be available through an API to everyone. So I think it’s very important, I think, to be able to have the capability to build the experiences that you want if you want to be one of the major companies in the world that helps to shape the future of these products.

Translation: in order to win in AI, I believe we need to own and control the entire stack, as it were. We can't rely on others' technology.

Two things stand out to me here:

- This mentality is clearly derived from Zuck's believe that Apple (and to a lesser extent, Google) has completely hamstrung Facebook and now Meta because they control the platforms on which he must operate.

- This is basically the opposite approach of the one Apple itself is taking with AI.

As mentioned, Apple also had banner earnings – their highest revenue and profit ever posted as the iPhone business came roaring back to life. The fact that it also led to a massive rebound in the China business, and you'd think investors would be over the moon. But again, unlike Meta's stock pop, Apple's after-hours results have been far more muted. In fact, the stock is currently down ahead of the market opening today.

There are a few likely reasons for this, but as Apple's own earnings call made clear, a big one is the concern around Apple's AI strategy.

You might think investors would love the fact that Apple has decided to largely outsource their work to Google. Not only is their frenemy viewed as a market leader, the partnership will ensure Apple can continue to keep their costs down relative to their peers. And when I say "costs down" – I mean literal fractions of the CapEx cost that Amazon, Google, Microsoft, and yes, Meta are spending.

Over the past year, Wall Street has rewarded this discipline at points, especially when they have viewed those other companies' spend as getting a bit out of control. But beyond Meta, Microsoft just saw their biggest single-day stock drop since the early panic around the pandemic in 2020. Why? Investors are worried about their CapEx spend! Obviously, it's a bit more nuanced – they're worried that Copilot isn't seeing the results from said spend and that Microsoft is still to overly reliant on OpenAI – but still, you'd think Wall Street would reward Apple for not following Microsoft's playbook here.

Instead, if anything, they might now be punishing them for not following Meta's strategy. Again, while investors initially liked the news that Apple was outsourcing their AI work to Google, if they're buying – quite literally – Meta's longer-term narrative here, then they're selling Apple's.

And the truly wild thing is that Apple is the company that's famous for wanting to own the entire stack! This is the Tim Cook doctrine! And he's implemented it to the point of harming Apple in the past, such as when he replaced Google Maps with Apple Maps early on in his tenure. He's clearly willing to pay short-term costs to ensure that Apple maintains long-term control over their technology.

But Apple, like Meta, failed in their first attempt at this with AI. The difference is that while Zuck doubled-down on their internal efforts, Cook doubled back.

To be clear, I think Apple is taking the correct approach right now. They simply don't have the time to completely rebuild their AI technologies in-house at the moment. Even if they could throw all of their money at the effort, like Meta is doing, they would have a hard time getting access to the NVIDIA chips required, with everyone else having those fully locked up. They could maybe partner with AMD or Google – which they clearly are and have been around TPUs to some extent – but it would still be months, if not well over a year before they had anything to show for it. And what that "anything" might look like, we'll see soon from... Meta!

Apple needed to reboot Siri yesterday. But the second best time to do so is today. The worst time is a year from now, given where others are likely to be by then. And that still speaks to a real risk here in partnering with Google. They might get the tech to cut to the front of the line, but if it's ever restricted, per Zuck's fears, they're going to potentially be in trouble...

And so they'll obviously keep working on their own systems behind the scenes, but without the AI being in operation in the real world, there's also a risk that they simply cannot catch up, ever. This was part of my argument for making a big AI acquisition – they did just make one, by the way, their second largest deal ever,1 but not related to foundation models – to both jump back into the game and get the talent on board to stay there. Basically, Meta's strategy with Scale and other such "hackquisitions".

In a way, this may all come down to timing. Meta clearly believes they need to be at the cutting-edge of AI right now. Apple clearly believes they can outsource the cutting-edge right now and wait and see how it develops. Again, that could end up being the more prudent move in the long run if, say, LLMs aren't the be-all/end-all of this all.

If it turns out that Zuck was spending hundreds of billions of dollars a year to build a technology that would end up completely commoditized... that will be a problem. Especially if Apple was spending something far closer to zero and was able to compete – or beat them from a product perspective. Obviously, we'll see.

Right now, Wall Street seems to be buying what Meta is selling while selling what Apple is buying. But it can and undoubtedly will switch again before we know the real answer. And that's fun because we'll all get to watch how it plays out – two opposite strategies by two hated rivals – in real time.

Thanks for reading, if you enjoyed this, perhaps:

🍺 Buy Me a Pint

🍻 Become a Monthly Member

🍸 Become a Yearly Member

1 At a reported $2B, it would be behind only the acquisition of Beats a dozen years ago at $3B. And yes, those are basically the size of hot AI seed rounds these days... I should also note/disclose that GV, where I was a GP for many years, was a seed investor in Q.ai. ↩